Passive ETFs: 4 Big Performance Problems, 2 Solutions

Exchange Traded Funds (ETFs) are heaped with praise (and continue to gain market dominance). The popular narrative is they provide dramatically better performance than actively managed funds (due to lower fees and less “unsystematic risk”). But in many cases, passive ETFs actually hurt investor returns more than they help. Here are four big performance problems with passive ETFs, and two bottom-line solutions.

Exchange Traded Funds (ETFs) are heaped with praise (and continue to gain market dominance). The popular narrative is they provide dramatically better performance than actively managed funds (due to lower fees and less “unsystematic risk”). But just as Fat Tony called Dr. John a sucker (see ludic fallacy) in Nassim Taleb’s famous Black Swan 100-coin-flip example, I’m saying passive ETFs actually hurt investor returns more often than they help. Here are four big performance problems with passive ETFs, and two bottom-line solutions.

1. Market Timing

ETFs make it easier for investors to trade in and out of the market with their entire portfolio anytime they want, and this “market timing” leads to dramatically worse returns (i.e. market timing is a bad idea). At least that’s what this old school study from 2013 (The Dark Side of ETFs and Index Funds) found. Specifically:

“individual investors worsen their portfolio performance after using these products compared with non-users…”

and the reason:

“is primarily due to bad market timing.”

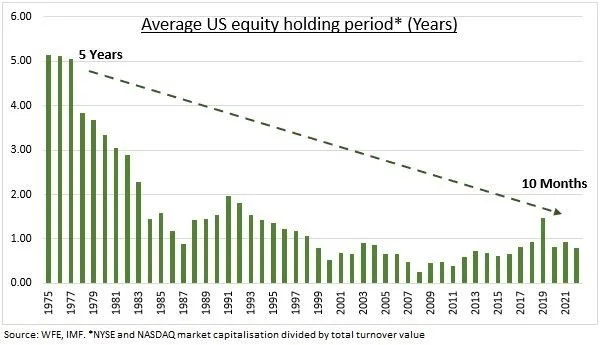

And considering the average investment holding period continues to shorten today (see charts below), I believe the market timing mistake is exacerbated by low-cost passive ETFs.

ETP is Exchange-Traded Product. Old data (2015) but still provides important perspective.

So in this case, the problem isn’t the low-cost passive ETF itself, but rather the bad behavior it enables.

2. Advisor Fees

Financial advisors are increasingly using passive market ETFs for clients (which may sound like a good thing), however they also continue to charge high fees.

For example, consider a financial advisor who charges a 1.5% annual fee to invest her clients in low-cost passive ETFs. Now compare that “fee-based” advisor to an old school “commission-only” advisor that uses mutual funds that charge a 0.75% annual fee, plus an upfront 3% sales charge (load) and an additional 0.25% annual sales charge to the advisor. That upfront sales charge might sound draconian, but if you do the math, after about 6 years it’s a wash (in terms of fees, assuming you’re a buy-and-hold investor) and over the long-term (more than 6 years) the mutual fund may actually be dramatically better for that investor’s bottom line (because the client ends up paying much lower fees).

Of course, good advisors do A LOT more than just pick investments (i.e. tax strategies, estate planning, wide-ranging financial discussions), but if they’re charging you much more than 1% per year—they’re probably charging you more than they’re worth (i.e. the passive ETF strategy (of said advisor) is actually hurting your returns again).

3. Niche ETFs

Investors often conflate the benefits of low-cost, passive market ETFs (such as Vanguard’s VOO and VTI) with specialized niche ETFs, and this can be a costly mistake. A lot of niche ETFs are focused on specific industries, styles, or gimmicks, and they typically charge much higher fees. What’s worse, these niche high-cost ETFs typically just provide overlap to what you already hold in VOO or VTI. The contsant loud praise for low-cost passive ETFs, combined with the proliferation of expensive niche ETFs, confuses many investors. It causes many to make bad decisions and often lowers their net returns dramatically.

4. Valuation Dying, Cryptocurrency Rising

A negative externality of passive ETF investing is that fundamental security valuations are increasingly disregarded to the detriment of investors. For example, this Financial Times article explains:

“In a system in which passive funds monopolise investment flows, the price of a security ceases to function as a gauge of a firm’s underlying prospects. This distorts the cost of equity and the price of credit.”

Said differently, when the market rises and falls it drags all securities held within an ETF higher and lower whether or not they are fundamentally good or bad companies. This can lead to bad companies being able to raise capital through debt and equity offerings when they shouldn’t be. And this is bad for the economy (and investors) because it increasingly leads to an inefficient allocation of capital (i.e. more defaults and losses that someone is ultimately on the hook for).

As another example, an entire generation of “investors” has absolutely no idea how to value an investment (because they just buy ETFs), and this disregard for valuation leads to the belief that cryptocurrency is an “investment” (even though it produces no earnings, pays no dividends and has zero physical value).

Further shirking responsibility, passive investing can give a lot of power to the large passive investment companies, such as BlackRock (i.e. iShares ETFs) who faces increasing legal and business pressures for arguably putting their political ESG views ahead of their fiduciary responsibilities (to the detriment of investor returns).

The 2 “Bottom-Line” Solutions:

First and foremost, you need to do what is right for you. That means don’t let your performance fall victim to market timing, don’t pay for an advisor that adds more fees than value, don’t shrink your total returns with expensive niche ETFs, and don’t forget that valuation does matter for investment markets to function efficiently.

And secondly, if you’re not comfortable doing it yourself, then the best investment advice is the same as it’s always been—work with someone you trust.

Are you Inheriting an IRA?

If you are inheriting an IRA, you’re going to want to know the rules. Here are 4 things to consider and 1 TLDR.

You’re going to want to know the rules.

Here are 4 things to consider and 1 TLDR:

Inherited IRA—If your Spouse Dies: If your spouse dies, and you are the sole beneficiary of his/her Individual Retirement Account (IRA), you can take over the account (i.e. spousal transfer/ “assuming” the IRA), and the IRS will treat it as though it has been yours all along.

You can even keep making contributions to the inherited IRA, and the schedule for required minimum distributions (RMDs) is reset so that it’s based on your own life expectancy.

Logistically speaking, you can either have yourself designated as the account owner, you can roll it over to your own IRA (assuming it’s the same type, Roth vs Traditional) or you can open a new IRA and roll the assets into that one. You can even take a lump sum distribution (just be mindful of the taxes).Inheriting an IRA from Your-NON Spouse: Did you know if you inherit an IRA from someone other than your spouse, you have to roll the assets over into a new account specifically designated as an “Inherited IRA”?

You can’t just roll the money into your own IRA b/c you may have to follow the Required Minimum Distribution (RMD) schedule based on the life expectancy of the deceased owner.

These same rules apply if the deceased is your spouse, but you are NOT the sole beneficiary of the IRA.The 10 Year Rule: Critically important, in most cases, if you inherit an IRA, you have 10 years (from the date of the account owner’s death) to deplete it (you can withdraw the money in any cadence or lump sum you want) (and this applies if the owner died after 12/31/19).

Just know, you have to pay ordinary income taxes on the withdrawals (unless you’re a minor, then the 10-year depletion clock may start when you turn 18. And if you’re not more than 10 years younger than the account owner, then you can stretch the withdrawals over your lifetime).The 5-Year Rule for Inherited ROTH IRAs: If you inherit a Roth IRA, you can withdraw the original owner’s CONTRIBUTIONS tax free at any time, but the EARNINGS on those contributions may be taxed if you withdraw them sooner than 5 years after the original owners death.

Also, critically important, even though Roth IRAs have no RMDs, inherited Roth IRAs do! (over the new owner’s lifetime). Any if you miss an RMD, the penalty can be as high as 50%!

TLDR: If your spouse dies, and you are the sole beneficiary of his/her IRA, you can take it over and the IRS will treat it as if it was always your IRA. If you’re not the spouse (or you’re the spouse but not the 100% beneficiary), then you have 10 yrs to withdraw all the money from the “inherited IRA” (exceptions apply, such as minors), and you will be taxed on the withdrawals as income. If it’s a Roth IRA, there are no taxes on withdrawals, subject to the 5 year rule on earnings (but not contributions) and you must take RMDs (or pay a hefty penalty).

GIFT TAXES: 4 Important Rules, 4 Mistakes to Avoid

If you’re so lucky to be giving and/or receiving “gifts” with BIG monetary value, you’re going to want to know the tax rules and common mistakes to avoid.

If you’re so lucky to be giving and/or receiving “gifts” with BIG monetary value, you’re going to want to know the tax rules and common mistakes to avoid.

4 Important Rules:

Annual Limit: You can give $18K per year in 2024 ($36K if you’re married) to as many individuals as you want, and you generally won’t be required to pay any gift taxes.

IRS Form 709: If you exceed the annual limits (above) then you have to file tax Form 709 to let the IRS know, but you still probably won’t have to pay any gift taxes.

Lifetime Exemption: There is a lifetime gift tax exemption of $13.61 million in 2024 (2x for married couples), but once you exceed that amount, you have to pay taxes on the gifts. The gift tax rate starts at 18% and climbs to 40% for gifts over $1 million (see table below). And the $13.61 million lifetime exemption reverts back to $5 million in 2026 if Congress doesn’t act.

Who Pays the Gift Tax? The giver of the gift pays it. Not the recipient. Just know that if someone gifts you stock (that they acquired years ago for $10) and you sell it (for $50) you pay income tax on the gain of $40 (Note: the rules are different if you receive the stock through an estate, then your cost basis is the mkt value of the stock on the day the previous owner died: this is the “stepped up cost loophole.”

4 Mistakes to Avoid:

You’re going to want to discuss your personal situation w/ your tax advisor first, but generally speaking, here are a few mistakes to avoid:

1. Gift the money before 2026: If you’re closing in on the $13.61 million lifetime exemption, you may want to consider gifting BEFORE the limit reverts back to $5 million in 2026 (although the gov will likely extend the higher exemption before then as a deal sweetener for some other gov money grab tbd at a later date). But there is no guarantee the higher limit gets extended.

2. Spread the gift out over multiple years. To avoid Form 709, you may want to consider spreading out large gifts (above $18K) over multiple years.

3. Don’t forget some states have estate taxes: Some states (such as New York, Illinois, and a handful of others) have their own estate taxes that kick in well below that $13.61 million federal exemption. For example, Illinois (the state I live in) kicks in for estates over $4 million and rises to 16% for estates over $10 million—yuck!

4. Don’t get sneaky: It’s not just cash that counts as a gift. Gifts can include cars, wedding expenses, vacations, loans (with no interest) and almost anything with value. However, there are exceptions (no gift tax) on tuition and medical expenses you pay for someone, as well as no tax on gifts to your spouse and gifts to a political organization. Also, gifts to qualifying charities are not taxed and may even be tax deductible.

The Bottom Line:

By knowing the gift tax rules, you can use them to your advantage and avoid costly mistakes. Be smart people!

How Many Stocks Should You Own?

25-30 stocks is the “magic number” to be diversified (according to a popular 1970 study by Fisher and Lorie) as you can see in the chart below (i.e. once you own 25-30 stocks, you’ve already diversified away the lion’s share of stock specific risk, from a standard deviation standpoint).

25-30 stocks is the “magic number” to be diversified (according to a popular 1970 study by Fisher and Lorie) as you can see in the chart below (i.e. once you own 25-30 stocks, you’ve already diversified away the lion’s share of stock specific risk, from a standard deviation standpoint).

“The Entire Market” View

And while the 25-30 stock number has been widely popular for decades, some academic types (i.e. nerds) believe standard deviation is the wrong metric, and 60 stocks is the bare minimum, but holding the ENTIRE MARKET is ever better (as you can see in the following table) when you consider “more prudent” metrics like tracking error and R-square.

source: Investopedia

Biased Opinions:

Of course there are huge biases (and conflicts of interest) by the people creating the studies. For example, many academics will push the maximum diversification story (i.e. just buy a market ETF and own ALL stocks) because they have little to no real world experience/skill and they personally are better off this way.

Similarly, many real world “sales people” with little to no actual investment experience/skill will also push the passive ETF story (because it’s easier for them and their business can generate more sales selling the passive ETF story).

Stock Picking & Portfolio Constructions Skills:

But what is actually true? The truth is, there are people with actual stock picking skill AND portfolio construction skill. It’s just really hard to identify and separate them from those winning through sheer luck (statistically, there should be a fair amount of lucky investors) and from those who are just really good sales people (whether they are inexperienced academics and/or unskilled CFP types, or fintwits bragging about their short-term luck as if it were skill).

Critically important as well, the chart and table above are all about eliminating “stock specific risk” so you are only left with “non-diversifiable” market risk. The problem with this is that they are based on the implicit assumption that no one has any stock-picking skill therefore you don’t want any stock-specific risk. The problem with this, of course, is that if you have stock picking skill (combined with prudent portfolio construction/risk management skill) you absolutely DO want stock-specific risk!

The Bottom Line:

If you are skilled, 25-35 stocks may be the right portfolio size, but only if you:

Sectors: Keep your portfolio weights roughly close to the market in terms of sectors (there are 11 GICS sectors, such as technology, consumer staples, materials, etc.).

Market Caps: Keep market cap weights (small, mid, large and mega-cap exposures) loosely similar to the market.

International: Consider adding a little international exposure too, but there are different opinions on this one. For example, Vanguard founder Jack Bogle didn’t really think international was necessary.

Style Exposures: Stay cognizant of the ebbs and flows of growth and value, especially in light of interest rate dynamics (i.e. keep your emotions in check as you invest for the long-term).

Specific Stocks: But most importantly, above all else, pick a few good stocks!

The long-term compound growth of just a little alpha snowballs into a lot of money over multiple market cycles.

Be smart people. Do what is right for you.